When I first heard of the Acorns investing app, I was intrigued and optimistic.

It sounded like a great option for beginner investors who wanted to get an easy start.

I decided to check it out myself, and my optimism quickly waned.

Here’s why I’d recommend staying away from this one.

1. The fee is too high for small investors

The Acorns app’s target audience is people who just want to invest small amounts at a time.

This is mainly accomplished via their “Round-Ups” feature, which detects when you make purchases, “rounds them up” to the nearest dollar, and invests the difference.

For instance, you buy a coffee for $2.50, and Acorns rounds it up to $3 and invests the 50 cents. Okay, not a bad feature (though I don’t know how I feel about an app watching all my purchases!).

Now, the Acorns app has a $1/month fee for their basic taxable investment account, or a $2/month fee for their retirement account.

It’s meant to sound low so you don’t really question it. However, it’s important to look at the percentages. The smaller a balance you have in your Acorns account, the larger percentage that monthly fee will be for you.

As a point of comparison, the average fee for a professional financial adviser is 1% of your balance annually.

Let’s do some example calculations using the $2/month fee (since a retirement account is a better idea for new investors than a taxable account).

- If you have $100 in your Acorns account, $24 a year is 24% of your balance.

- If you have $200 in your account, it’s 12%.

- If you have $500, it’s about 5%.

- If you have $1000, it’s 2.4%.

As you can see, the Acorns cost doesn’t start to become a competitive rate unless you have several thousand dollars to invest.

Acorns reports that their average investor puts in $32/month, or $384/year. In this case, it would take that average investor 5 years for the fee to get low enough to equal 1% of their balance.

And given that you could sign up for Wealthfront and have your assets managed for free up to $5,000, and a 0.24% balance fee after you exceed $5k…

I certainly wouldn’t call the Acorns cost low at all when you compare it to the industry.

Related posts:

2. They’re slimy about referral rewards

Acorns regularly advertises the opportunity to earn more in bonuses through referrals—for instance, $500 for referring 5 people in a month, or $1000 for referring 12 people.

This sounds pretty good, right? Almost…too good to be true?

Here’s my experience. I decided to go for one of the $500 for 5 people incentives.

I told 5 family members and friends about the app and walked them through the process of signing up.

The plan was to share the bonus with them once it was paid so everyone would have a healthy start to their accounts.

The referrals took a while to show up in my account, and they displayed as “Pending” for a long time. A month went by with no bonus.

I contacted Acorns customer support.

They recommended having the 5 people I’d referred get in touch to confirm they had been counted.

Okay, that’s a pain, but they did.

Another month passed, so I got in touch again.

This time, they claimed that only 4 of the 5 people had actually used my link to sign up.

First of all, I was actually with them to help, so I know they did use the correct link.

Also, keep in mind that all five people had contacted Acorns customer service to confirm that I had referred them.

They didn’t care, refused to count the fifth person, and instantly lost my respect and support.

If a referral was not recorded due to a tracking problem on their end, that should be their responsibility to fix. They did not.

After this happened, I looked through their Facebook page reviews, and found other people with the same experience.

To me, this looks like a clear pattern of false advertising and deceit.

Now, some people have reported that they were paid their bonuses—so perhaps Acorns has a set monthly bonus budget, approves enough people to avoid looking like a total scam, and stiffs the rest.

Either way, the whole experience has left an incredibly sour taste in my mouth about Acorns customer service and the company as a whole.

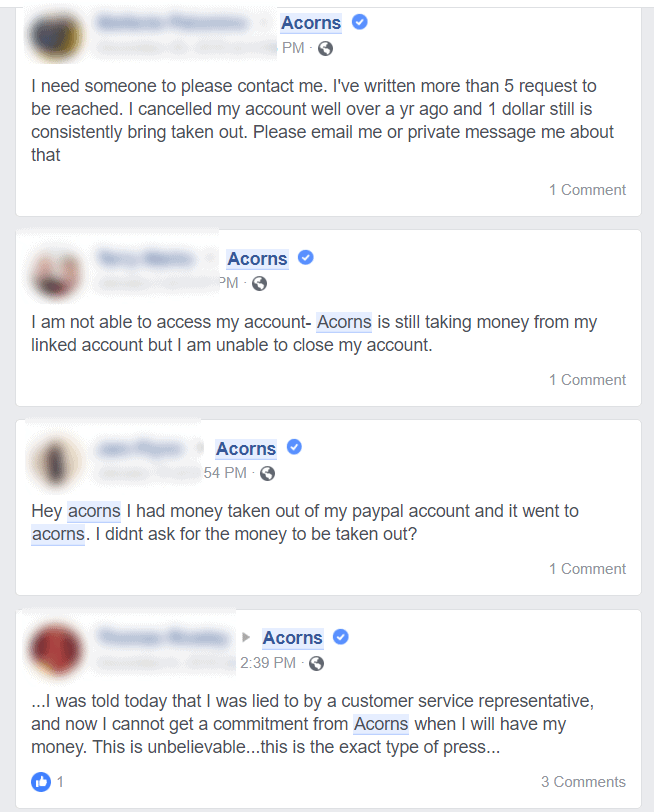

3. Acorns withdrawal time: People have reported difficulty withdrawing their money

I haven’t tried to close my account yet, so I can’t speak from personal experience on this one.

However, in my research I found enough people complaining about this that, again, it doesn’t look like a fluke.

People have had difficulty getting their money from Acorns withdrawals, and in some cases, they’ve even continued being charged the monthly fee after they’ve canceled their accounts.

Here’s a small sample of what users have been reporting:

This is a big, big problem. Being lied to about referral incentives is one thing, but not being able to withdraw your own money?

Being charged after you’ve canceled your account?

I truly wouldn’t be shocked to see Acorns in legal trouble soon if they keep this up.

4. Disorganized and non-transparent customer service

After essentially being told “too bad” by customer service when I attempted to resolve my issue, I contacted a few other people to get their stories.

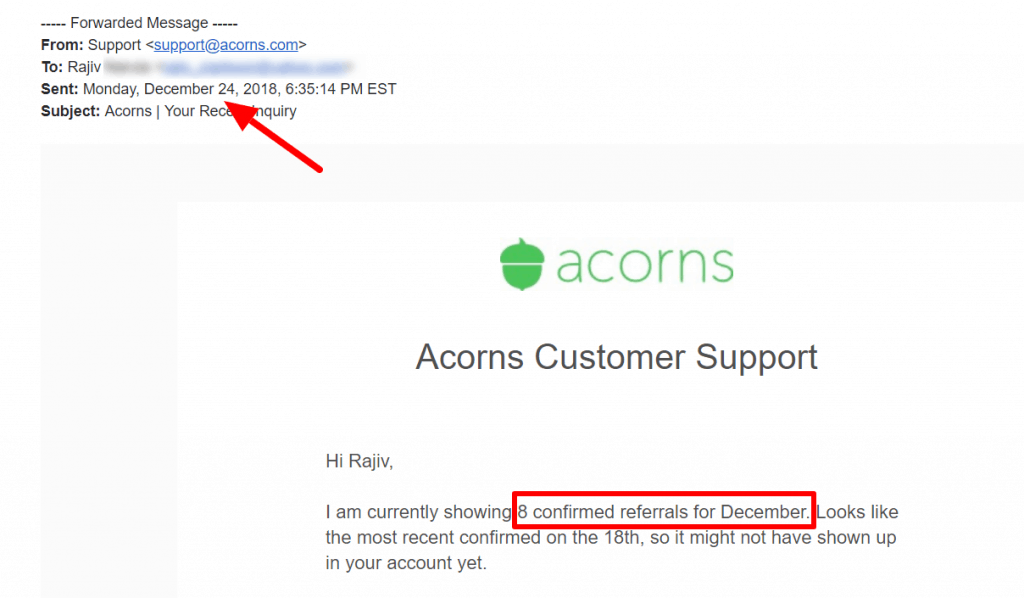

One of them, Rajiv, had quite an interesting saga of dealing with customer service.

He was dealing with the same issue I was—he had referred 12 people for an incentive, but some of their accounts had gone into a limbo.

Even better?

He had the emails to show Acorns customer service literally contradicting themselves, and he kindly agreed to share them for the article.

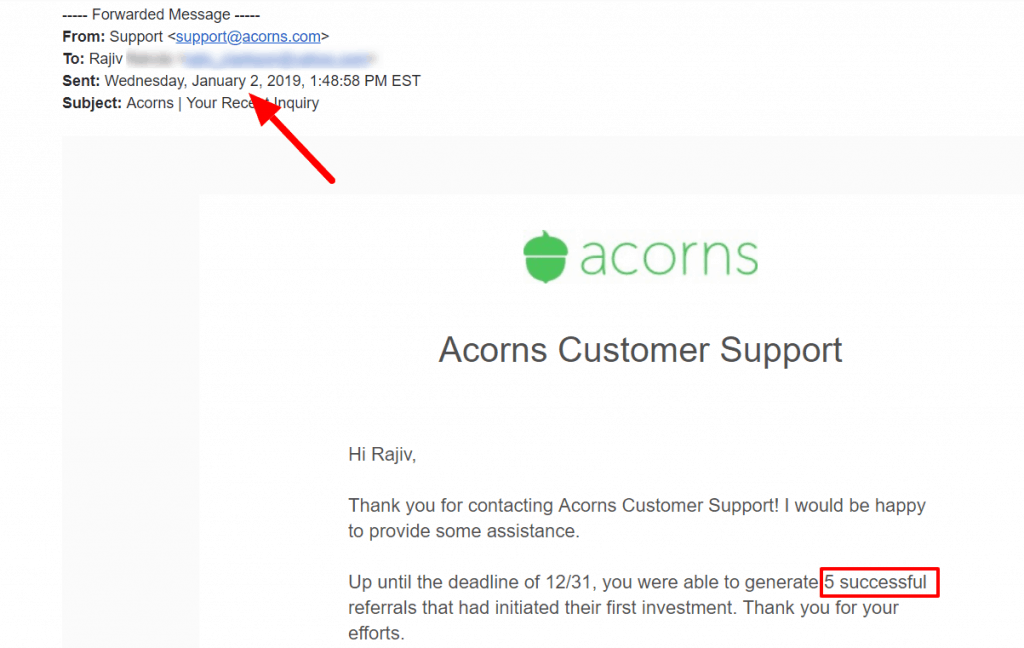

Let’s take a look, shall we? Here’s an email from December 24, 2018 where they tell him he has 8 confirmed referrals for December:

And here is an email over a week later, on January 2, 2019, claiming that he only has 5 confirmed referrals for December:

Interesting how 3 successful referrals could just disappear, isn’t it? Rajiv informed me that his friends had also been calling Acorns to confirm that they should have been recorded.

“Thank you for your efforts” is all he got.

I’d like to clarify that I don’t blame the customer service people themselves here.

I think they’re innocent people working for an ill-managed company, just trying to earn a paycheck.

Dealing with frustrated people all day is probably pretty frustrating too, especially when you don’t have the power to actually help them. I wish these people luck.

So, my final thoughts…the Acorns app was a good idea in theory, but it seems to be pretty terrible in practice.

I hope this review helps a few more people avoid being sucked in.

Since they’re really targeting beginners who don’t have much investment experience, I would hate for a bad Acorns investing experience to turn people off the stock market altogether.

Want better ideas on how to invest?

As I mentioned above, I’d recommend Wealthfront for automated, hands-off investing. It’s where I keep my Roth IRA, and I’ve had no problems.

It’s not exactly in the same category as apps like Acorns (e.g. they don’t have a round-ups feature), but it’s still very simple to use.

For more on that and other options, check out my full article on how to invest without being a stock market expert.

Kate is a writer and editor who runs her content and editorial businesses remotely while globetrotting as a digital nomad. So far, her laptop has accompanied her to New Zealand, Asia, and around the U.S. (mostly thanks to credit card points). Years of research and ghostwriting on personal finance led her to the FI community and co-founding DollarSanity. In addition to traveling and outdoor adventure, Kate is passionate about financial literacy, compound interest, and pristine grammar.

I was turned off by Acorns by their fees alone. I’d rather get some sort of cash back a la Dosh or Drop and invest that money than have my purchases rounded up, anyway.

I haven’t used Dosh or Drop yet! I’ll give them a try for sure.

Thanks for sharing. I actually really enjoyed Acorns so far and I shop at Sam’s Club every week which means I get back $1 in ‘Found Money’ so the fee is more than covered.

I didn’t know they had so much shadiness with the fees and withdrawals. I’ve got about $600 with them. I’ll probably try to withdraw it and see what happens.

I liked it well enough at first too, until I had that weird referral experience and started digging. If it’s paying for itself with the Found Money, you might want to keep it around for that, but I definitely wouldn’t trust them with keeping much of your own money in there. It seems like people who do have problems really struggle to get them resolved. Hope the withdrawal doesn’t give you problems!

Another commenter suggested the apps Dosh and Drop for a similar “found money” feature, so I plan to try those next.

Wow, this is a detailed review and raises a lot of red flags. I haven’t used Acorns but I have found that there are so many of these new fintech services popping up, it’s hard to keep up. I was looking into Realty Shares for a while and then before pulling the trigger, poof — the site is gone. Now it wasn’t anything wrong with the service, per se, but the company didn’t raise enough money to keep going. So it’s hard to know what to invest, not just your money, but also your time and energy into. I have mutual funds and real estate. My funds are with Vanguard — reliable for a long time and not going anywhere soon. Real estate is owned directly so not REITs or crowdfunding. This creates more paperwork but also more control.

Crazy that the site just disappeared. Sticking with more established companies is probably the wisest course of action at the end of the day!

Can’t withdraw I paused my weekly pay ins and it was still charging my account sending into over drawn status costing me $35 each charge they’d charge me 2 times back to back. Tried to withdraw my account was locked upon trying to withdraw… Shady ass company. Probably have to change my account numbers and everything to keep it from happening again.

Whatever- it’s simple, easy, and I’ve withdrawn $ previously without issues. My returns have been quite good over the past 4 years, and I have far more $ in it now than I would have imagined.

Share how you withdraw your money… I have sent email after email with no response.

This is a great piece, Kate. I’ve never considered using the Acorns app, but this is definitely an eye-opener for why it may not be the best for some people.

Maybe their referral service is just like that because it’s the internet and they have to be wary of scammers, so if anything looks shady, they immediately deny it. Never really had problems with Acorns but their found money detection needs some work. I used the Found Money links for Blue Apron, Enterprise car rental and Hotels.com and so far, I’ve only gotten credit for the Blue Apron; the Enterprise and Hotels.com purchases just vanished into thin air even though I started the purchase process from the website AND had the acorns Chrome extension enabled. I haven’t contacted them about it yet, but I’m doing so today. I’m not concerned with the fees because it’s easy to pay for it just with Found Money that I spend on things that I was going to buy anyway. I got $35 from my Blue Apron purchase which, according to your chart for accounts with only $100, that’s enough to cover me for a little over a year. As far as withdrawing, I only had to withdraw once and my money was back in my bank account at the same speed as a regular bank account transfer.

I opened an account with $1000 and closed it shortly after on Aug. 2, 2019. The claim it may take up to but no longer than 9 days to return your money. It’s now August 22 and still no returned funds. I have emailed customer service three consecutive days with zero response. Going to try a call today and then file a complaint with the SEC on Monday if I don’t get resolution. STAY AWAY from Acorns. No excuse for this level of bad customer service and adherence to their own policies.

That’s really unacceptable. Filing a complaint is a smart next step.

I always have thought that Acorns wasn’t that good. I’ve googled the reviews and all I get are bloggers giving you their reviews but keep in mind they are getting paid for their review. You are the first real honest review I have found. I think I’ll pass on Acorns. Sounds like shady things going on with them